If payments fail in emerging markets, I do not start with cards or checkout UI alone. I look at three things first: integration errors, issuer or wallet declines, and local price fit.

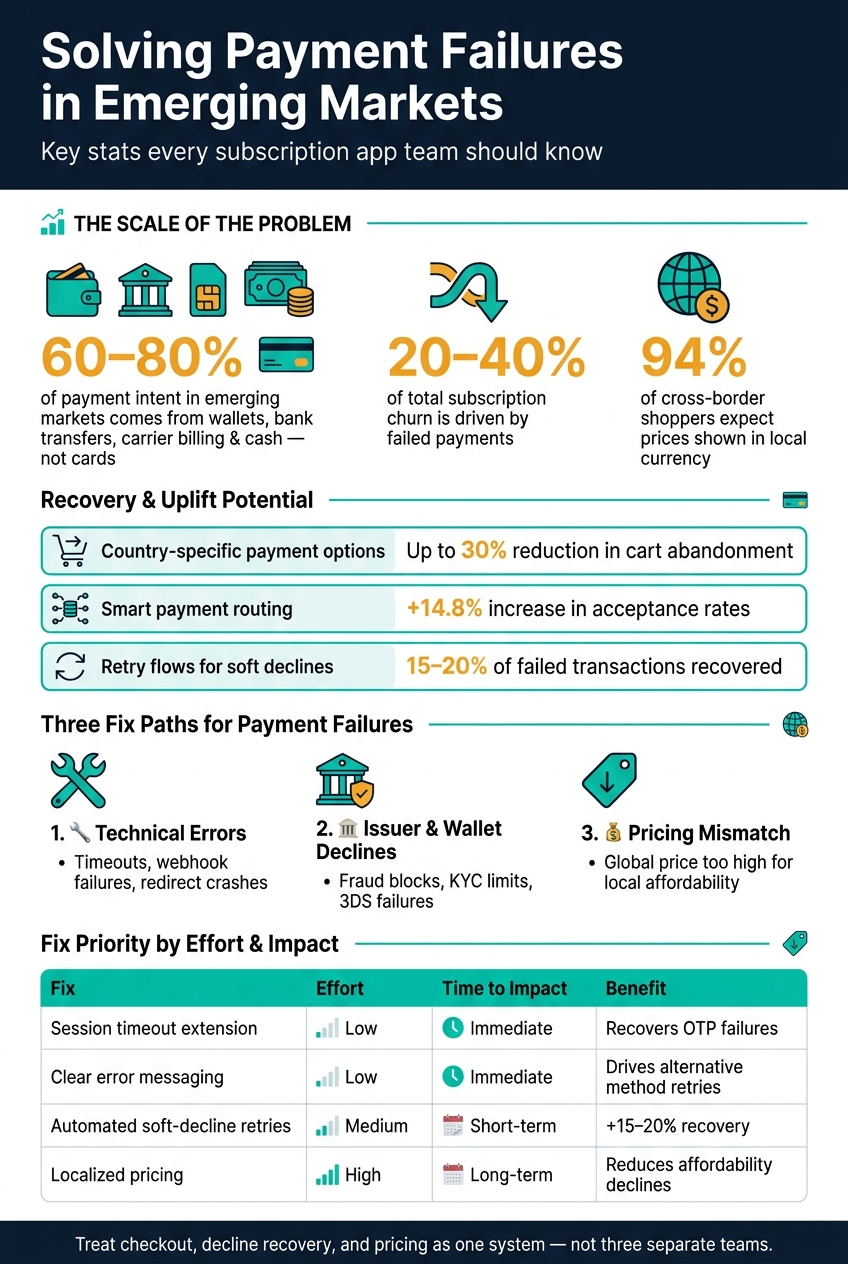

In many of these markets, cards are not the main path. Wallets, bank transfers, carrier billing, and cash-based networks can drive 60%–80% of payment intent. That changes the job. If I rely on a U.S.-style card flow, ignore redirect and webhook edge cases, or keep one global subscription price, I should expect lower conversion, more failed renewals, and more involuntary churn.

Here is the short version:

- Fix the stack first: idempotency, webhook handling, redirect recovery, timeout windows, and checkout crash tracking

- Treat declines by type: retry soft declines, avoid blind retries on hard declines, and time retries around local pay cycles

- Localise payment methods: put the top local rail first, not behind card entry

- Localise pricing: if “insufficient funds” stays high, the issue may be the price, not the rail

- Measure by country and method: aggregate success rate hides where revenue is leaking

- Use the right layer for the right job: Mirava helps decide what to charge by country, while RevenueCat, Adapty, Purchasely, and Superwall handle billing, entitlements, and paywall delivery

A few numbers make the point clear:

- Country-specific payment options can cut abandonment by up to 30%

- Smart routing can lift acceptance by about 14.8%

- Retry flows can recover 15%–20% of soft declines

- Failed payments can drive 20%–40% of subscription churn

- 94% of cross-border shoppers expect local currency display

If I want fewer payment failures, I need to treat checkout, decline recovery, and pricing as one system - not three separate teams working in isolation.

Payment Failures in Emerging Markets: Key Stats & Fix Impact

The main causes of payment failures

Not all payment failures come from the same place. The first step is to split them into three fix paths: technical errors, downstream declines, and pricing mismatch. That split matters because each one calls for a different response.

Technical and integration failures

Technical failures happen at the infrastructure layer. Think timeouts on weak mobile networks, the OS killing the app during a bank redirect, or webhook failures caused by missing signatures or out-of-order delivery on asynchronous rails. A good practice here is to map rail-specific errors into one internal code system, while still keeping the raw error available for debugging.

The fix is usually clear:

- Use idempotency keys on every API call and webhook so retries don’t lead to double-processing

- Run regional health checks to spot outages that never show up in staging

- Add crash monitoring on checkout screens, not just across the app as a whole

These are resilience issues. Swapping payment methods won’t solve them.

Bank, carrier, and wallet declines

These failures come from the bank, carrier, or wallet. In dashboards, they can look almost identical. In practice, they’re not. Fraud blocks on foreign merchants, KYC tier limits on mobile money accounts, 3DS authentication failures caused by delayed OTP delivery, and session expirations inside wallet apps each need a different recovery path.

The table below maps common decline reasons to decline type and the best next step:

| Failure Reason | Decline Type | Common Trigger | Best Recovery Action |

|---|---|---|---|

| Insufficient Funds | Soft | Low wallet/bank balance | Trigger dunning or prompt user to top up |

| Fraud Block | Hard | Foreign merchant ID | Suggest a local payment method (e.g., Pix, UPI) |

| KYC Tier Limit | Hard | Transaction exceeds user's daily limit | Prompt user to upgrade KYC or use a different method |

| 3DS Failure | Hard | Incorrect OTP; carrier delay in SMS | Offer a non-card alternative or retry authentication |

Soft declines can often be recovered. Hard declines usually can’t. If the recovery step doesn’t match the decline type, retries just burn revenue and user trust.

Affordability and pricing mismatches

A flat global price can show up as "Insufficient Funds" when the real issue is local affordability. If that decline reason is high compared with other decline types, that’s a strong sign the price point is above local willingness to pay, or that retry timing ignores local payday cycles. In those cases, checkout fixes won’t bring the sale back.

The pattern is simple: these three causes lead to three different fix areas - checkout resilience, recovery logic, and regional pricing.

sbb-itb-43fe43a

Solutions that cut failures before and after checkout

These fixes line up with the three failure buckets above: method coverage, soft-decline recovery, and localisation.

Support local payment methods and build resilient checkout flows

Start with payment method coverage. In emerging markets, local rails often drive 60–80% of consumer payment intent, while cards sit in the long tail [2]. That has a direct effect on conversion: offering country-specific payment options can cut cart abandonment by up to 30% [8].

The catch is the plumbing. LPM integrations need stable error handling, clean webhook processing, and sandbox environments that behave like production. If those basics are shaky, checkout breaks in ways teams struggle to trace [2].

A few market examples make the pattern clear:

| Country | Dominant Method | Common Failure Mode | Mitigation Tactic |

|---|---|---|---|

| Brazil | Pix | QR code expiry | Extend auth window; send payment link via SMS [7][8] |

| India | UPI | Bank server timeouts | Use UPI Intent flow; multi-gateway routing [5][3] |

| Saudi Arabia | Mada | Cross-border block | Route through local acquiring partners [1][7] |

It also helps to stretch session timeouts to 5–6 minutes so users have enough time for OTP steps and bank auth delays [3][5]. Put the fastest local wallet first, not buried under card entry. Checkout should also filter payment methods on the fly based on the shopper’s country, currency, and transaction limits [8].

This is where the stack tends to split. Tools like RevenueCat, Adapty, and Purchasely help downstream with billing and paywall execution. Mirava sits upstream, looking at pricing and market signals so teams can decide which payment and price setup makes sense before traffic ever hits the paywall.

Once the right method is in place, the next job is fixing the retry path.

Use dunning, retries, and grace periods to recover soft declines

Not every failed payment should be retried. Focus on soft declines, then retry 2–4 times over 7 days, timed around local pay cycles. That approach usually recovers 15–20% of failed transactions [3][5]. Given that failed payments drive 20–40% of total subscription churn, that recovery rate matters more than most teams think [10].

RevenueCat and Adapty can manage billing logic and entitlements, while Purchasely and Superwall can support paywall flows and recovery messaging [8]. On top of that, dunning should start before the charge fails. Notify users about expiring cards 30, 15, and 7 days before expiration to cut avoidable failures [10].

A simple rule works well here:

- Retry soft declines

- Skip hard declines

- Align retry timing with local salary dates and bank behaviour

- Keep a short grace period so users don’t lose access the moment a payment hiccups

That mix tends to save revenue without creating a messy user experience.

Localize error handling and paywalls by country

Even when the payment flow itself works, poor error handling and generic paywalls still push users out.

A vague “Payment Failed” message leaves people stuck. A message with a next step performs better - "Your bank is temporarily unavailable - please try UPI or net banking" [3][5]. That kind of copy reduces friction because it tells the user what to do now, not just what went wrong.

Pricing display matters too. Show prices in local currency, since 94% of cross-border shoppers expect it [8]. And don’t just test paywalls on top-end devices. Mid-range Android phones are still the default in many markets, and smaller screens can cut off currency symbols or localised copy at the worst possible moment.

For teams working across markets, this is less about one-off translation work and more about country-level fit: local payment method, local price display, local failure message, and device-tested paywalls that hold up under normal conditions.

How pricing strategy can reduce payment failures

In emerging markets, price itself can cause payment failure even when the payment rail is working. That means pricing sits inside payment reliability, not just monetisation.

Replace global default prices with country-level price points

A straight exchange-rate conversion often lands on local prices that are simply too high for how people buy in that market. If a price takes up more than a market can comfortably support as a share of income, that’s a pricing issue, not a billing issue.

A locally calibrated price can lift conversion and retention in a material way [4]. In practice, that means setting prices around local purchasing behaviour: using shorter billing periods where monthly cash flow is tight, offering lighter entry tiers to reduce the first-payment hurdle, and setting country-level price points that match what users can actually keep paying.

Use Mirava as the pricing intelligence layer

Mirava sets country-level prices using real digital purchasing behaviour, while RevenueCat, Adapty, Purchasely, and Superwall handle billing, entitlements, and paywalls. Mirava answers what to charge; the billing and paywall stack handles how to charge and present it.

Once the right price is in place, the job shifts to getting that price cleanly into billing and paywall systems.

Build a pricing and billing workflow that scales

Use one workflow: set price in Mirava, publish to app stores, sync to billing, and test paywall presentation.

| Layer | Primary job | Example tools |

|---|---|---|

| Pricing intelligence | Determine country-level price points based on local purchasing behavior | Mirava |

| Billing & entitlements | Apply the selected price in subscriptions and access control | RevenueCat, Adapty |

| Paywall & experimentation | Localize and A/B test seasonal pricing presentation and paywall flow | Purchasely, Superwall |

Pricing should be treated as a recurring input, not a one-time launch task. In markets with fast-moving exchange rates or inflation, a locally calibrated price can go stale fast. When that happens, affordability-driven declines can creep back in quietly, along with abandonment and renewal loss.

Measure results and prioritize the highest-impact fixes

Track the metrics that show where revenue is leaking

Once checkout and pricing are fixed, the next job is simple: find the failures that still cost you money. A single payment success rate won’t do much here. It smooths over the patterns that matter, especially by country and payment method. You need to break payment success rate, decline rate, and failure reasons into the same segments: country, payment method, subscription stage, and time of day[5].

That level of detail is where the leak usually shows up. A card flow might look fine in aggregate, then fall apart for renewals in one market during a certain bank processing window. If you don’t segment, you miss it.

Split payment failures into hard declines, soft declines, and technical errors. Only soft declines can be recovered through retries[3][5]. Technical issues such as API timeouts, webhook failures, and gateway downtime need their own tracking line[10]. Don’t mix them with issuer declines or customer-side payment issues, or the picture gets muddy fast.

Two metrics often get less attention than they should: involuntary churn and renewal recovery rate. Failed payments can drive 20%–40% of total subscription churn, so it pays to measure how many failed renewals later recover through retries[10]. That’s the difference between seeing a failed charge and seeing its downstream revenue cost.

Also track checkout drop-off before the payment attempt. If users leave before they even try to pay, the issue is often pricing or affordability, not billing friction[6]. That’s a useful signal for teams using RevenueCat, Adapty, or Purchasely on the billing and paywall side, because it points upstream to pricing logic rather than checkout mechanics. This is exactly where a pricing intelligence layer like Mirava adds value: not at the point of billing execution, but earlier, where price positioning shapes conversion.

Prioritize fixes by revenue at risk and ease of implementation

Once the metrics are in place, rank fixes by revenue at risk and implementation effort. Estimate monthly revenue at risk first, then sort by recovery potential and build effort[3][5]. In practice, the order should follow the source of failure: infrastructure first, declines second, pricing third.

Start with integrations. Session timeout extensions, missing idempotency keys, and webhook gaps are usually low-effort changes with fast impact[3][9][10]. These are the sort of fixes that remove avoidable payment loss without needing a broad product change.

After that, move to recovery flows. Automated retries for soft declines and routing around weak banks or issuers tend to deliver a solid lift at medium effort. Smart routing alone has been shown to drive an average 14.8% increase in acceptance rates[3][5]. If you’re operating across regions, this matters even more, because bank uptime and issuer behavior vary a lot by market.

If decline patterns keep pointing back to affordability, then pricing becomes the bigger lever. That’s usually a higher-effort move, but the payoff can be larger as well[4]. In those cases, the issue isn’t that the payment stack failed. It’s that the price point failed before the transaction had a fair shot. For subscription apps selling across markets, that often means moving beyond flat global pricing and using local willingness-to-pay data to optimise price by region.

| Fix Category | Effort | Time to Impact | Primary Benefit |

|---|---|---|---|

| Session timeout extension | Low | Immediate | Recovers OTP-related failures[3][9] |

| Clear error messaging | Low | Immediate | Encourages retries with alternative methods[3][5] |

| Automated retries | Medium | Short-term | Recovers 15%–20% of soft declines[3][5] |

| Smart routing | Medium | Short-term | Bypasses bank downtime; +14.8% acceptance[3][5] |

| Localized pricing | High | Long-term | Reduces affordability-driven declines[4] |

FAQs

How do I tell if failures come from pricing or payments?

Review your payment gateway failure reports and group issues by reason code. Technical errors such as bank timeouts, session expirations, or network latency usually point to payment flow or integration friction. If those handoffs go through but users still drop off at the price screen, the problem is more likely pricing.

Use Mirava to optimise region-specific pricing, then rely on RevenueCat, Adapty, Purchasely, or Superwall for billing, paywalls, and entitlements.

Which local payment methods should I prioritize first?

Prioritize the payment methods with the highest local market share. In many emerging markets, cards account for only a small slice of transactions.

Start with trusted, everyday options like Pix in Brazil, UPI in India, mobile wallets such as GCash and JazzCash, and local bank-transfer systems like iDEAL or BLIK. Mirava helps set region-specific pricing, while RevenueCat, Adapty, Purchasely, or Superwall handle billing and paywalls.

What should I fix first to reduce involuntary churn?

Start by auditing transaction failure reasons so you can split retriable issues from non-retriable ones. That gives you a clean view of what can be recovered and what needs a different fix. For soft declines, add automated retries with exponential backoff. Use idempotency keys as well, so a retry doesn’t turn into a duplicate charge.

It also helps to tighten up checkout. Cut extra steps, support local payment methods, and show clear error messages that tell the user what to do next instead of leaving them stuck. Tools like RevenueCat, Adapty, Purchasely, and Superwall can support billing flows and entitlements, while Mirava sits upstream as the pricing intelligence layer, helping teams set the right region-specific pricing.