If you compare the wrong trial setup, your benchmark is wrong from the start. I’d use trial model first, category second, and region third when judging free trial performance in 2026.

Here’s the short version:

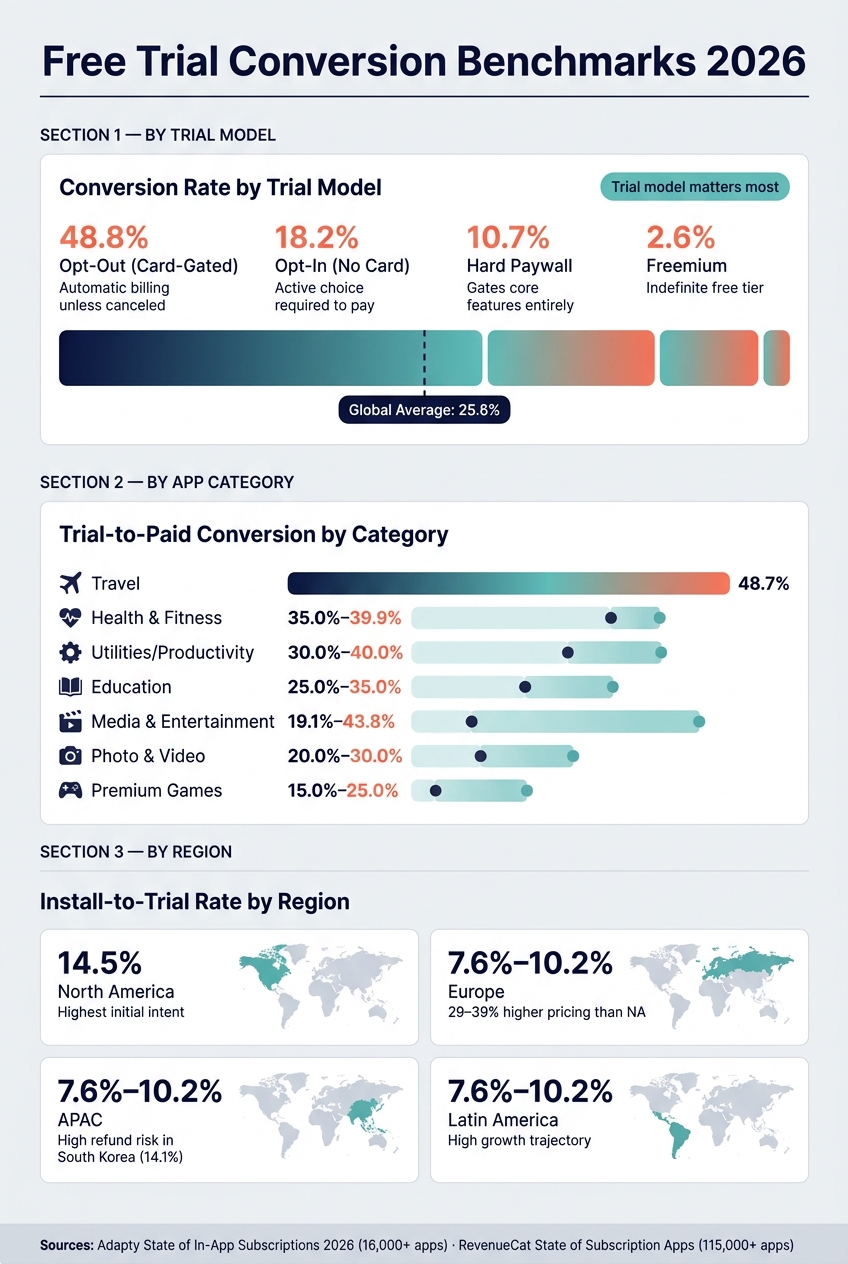

- The global average trial-to-paid rate is 25.6%

- Card-gated opt-out trials convert at 48.8%

- No-card opt-in trials convert at 18.2%

- Freemium converts at 2.6%

- Travel leads category benchmarks at 48.7%

- Health & Fitness sits around 35.0%–39.9%

- Utilities/Productivity lands at 30.0%–40.0%

- Media & Entertainment has the widest spread at 19.1%–43.8%

- Longer trials of 17 to 32 days reach 42.5%, versus 25.5% for trials of 4 days or less

- North America leads install-to-trial at 14.5%, while Europe, APAC, and Latin America sit around 7.6%–10.2%

What I take from this is simple: a headline average is not enough. A 35% conversion rate can look weak or strong depending on the category, billing setup, pricing, and payment access in each market.

| Lens | What I’d check first | Why it matters |

|---|---|---|

| Trial model | Card-gated, no-card, hard paywall, or freemium | This changes conversion more than anything else |

| Category | Travel, Health & Fitness, Utilities, Media, and others | User intent and value timing vary a lot |

| Region | North America, Europe, APAC, Latin America | Price tolerance, cards, and refunds shift results |

| Measurement window | Trial end vs. Day 35 / 30 / 60 days | The same metric can mean different things |

| Pricing | Local monthly and annual price points | Bad local pricing can hurt conversion before billing starts |

I’d also keep the data sources separate. Adapty and RevenueCat are both useful, but they track different app bases and use different measurement rules. And if I were reviewing performance in tools like RevenueCat, Adapty, Purchasely, or Superwall, I’d still want a pricing layer upstream. That’s where Mirava fits: helping teams analyse local price fit before they optimise paywalls and billing flows.

Below, I break down the benchmark ranges that matter most and how I’d read them in practice.

Free Trial Conversion Benchmarks 2026: By Model, Category & Region

What's a Good Trial Conversion Rate? (The App Marketing Sales Funnel)

sbb-itb-43fe43a

2. 2026 free trial conversion benchmarks by app category

The 25.6% global benchmark [3] hides a big gap between categories. The clearest differences show up in Health & Fitness, Utilities/Productivity, and Media & Entertainment.

Health & Fitness, Media & Entertainment, and Utilities

Health & Fitness sits above the overall median, with a 2026 range of 35.0% to 39.9% [3][7]. Top-quartile apps in this category clear 50% [1]. That pattern makes sense. If a product builds a routine fast and pushes users toward annual plans, conversion tends to hold up.

Utilities/Productivity apps land in a similar band of 30% to 40% [1]. These apps often convert well for a simple reason: users can judge the value in the first session. If the app saves time, fixes a pain point, or removes friction right away, the pay decision comes early.

Media & Entertainment is the most volatile category in the dataset. It ranges from 19.1% to 43.8% [2][3]. That spread usually comes down to content depth and trial exhaustion. Some users arrive with low intent, binge during the trial, then cancel as soon as billing kicks in.

Travel and broader subscription app segments

Outside those core categories, Travel stands out for a different reason: urgency.

Travel apps lead the market with a median trial-to-paid conversion rate of 48.7% [2][7]. The value is tied to a specific trip, so intent is high and the window to act is short. In practice, that tends to produce cleaner conversion than categories where users can delay the decision.

At the other end of the range, Premium Games and Photo & Video tend to sit below the median. Premium Games land in the 15% to 25% range [1], while Photo & Video sits between 20% and 30% [1]. Both face heavy pressure from free options. Photo & Video also sees higher refund rates in APAC, which can drag down paid conversion quality even when top-line trial starts look healthy.

| Category | 2026 Median Range | Notes |

|---|---|---|

| Travel | 48.7% [2][7] | High intent; time-bound value |

| Media & Entertainment | 19.1%–43.8% [2][3] | Content depth drives the spread |

| Health & Fitness | 35.0%–39.9% [3][7] | Habit formation; annual plans dominate |

| Utilities/Productivity | 30.0%–40.0% [1] | First-session utility; high intent at install |

| Education | 25.0%–35.0% [1] | Value builds over time; longer trials help |

| Photo & Video | 20.0%–30.0% [1] | High competition; elevated refund rates |

| Premium Games | 15.0%–25.0% [1] | Low commitment; heavy free alternatives |

Next, region and trial model show where the same category converts differently.

3. 2026 free trial conversion benchmarks by region and trial model

Category benchmarks only get you so far. User location - and the way the trial is set up - often explains the rest.

Regional benchmark ranges: North America, Europe, Latin America, and APAC

Regional conversion shifts mostly because of pricing tolerance and payment infrastructure, not simply market size.

North America has the highest trial-start rate [6]. That gives apps a head start before paid conversion even comes into play.

Europe tends to be priced higher. Apps in European markets usually charge 29% to 39% more than comparable apps in North America [3], and the UK, France, and Germany index about 20% higher on pricing willingness than the U.S. baseline [5].

Latin America includes some of the fastest-growing markets in 2026, but install-to-trial rates still sit in the lower benchmark band [6].

APAC has a different issue: refund exposure in some markets. In South Korea, Photo & Video apps can see trial refund rates as high as 14.1%, compared with a 6.4% global average [6]. That weakens paid conversion quality even when trial starts look solid.

| Region | Install-to-Trial Rate | Notable Factor |

|---|---|---|

| North America | 14.5% [6] | Highest initial intent |

| Europe | 7.6%–10.2% [6] | 29%–39% higher pricing than North America [3] |

| APAC | 7.6%–10.2% [6] | High refund risk in South Korea (14.1%) [6] |

| Latin America | 7.6%–10.2% [6] | Lower trial-start rates; high growth trajectory [3] |

Trial structure then changes those regional baselines again.

Trial model differences: opt-in, opt-out, freemium, and card-gated

The way you design the trial can change conversion by a wide margin, so direct comparisons across models can be misleading. The table below shows the main conversion ranges by model.

| Trial Model | Trial-to-Paid Conversion | Commitment Level |

|---|---|---|

| Opt-out (Card-gated) | 48.8% [2] | High - automatic billing unless canceled |

| Opt-in (No Card) | 18.2% [2] | Medium - active choice required to pay |

| Hard Paywall | 10.7% (D35) [9] | High - gates core features entirely |

| Freemium | 2.6% [2] | Low - indefinite free tier, no fixed window |

Trial length matters as well. Trials running 17 to 32 days show a median trial-to-paid conversion of 42.5%, versus 25.5% for trials of four days or less [9][2]. Even so, 46.5% of apps still use trials lasting four days or less [2][4].

How pricing affects regional conversion rates

Pricing can either support conversion or choke it off, even when user intent is there.

A subscription priced at $12.99/month in the U.S. is the global median [3]. In India, where the regional pricing index is about 0.6x the U.S. baseline [5], that same price adds friction before the trial even begins. Card-gated trials are tougher to run there too, since card penetration is only 8% [2]. That’s why local payment rails such as UPI Autopay matter.

Teams looking at these regional gaps often use a pricing intelligence layer like Mirava to analyse country-level price points based on actual digital purchasing behaviour. Those prices can then flow downstream into billing and paywall tools such as RevenueCat, Adapty, Purchasely, and Superwall.

4. How the 2026 benchmarks were measured

Metric definitions and conversion windows

The measurement windows here matter more than they might seem at first glance. They’re the reason the category and regional benchmarks above shouldn’t be compared like-for-like.

Strict trial-to-paid conversion measures the share of users who start a free trial and then move into a paid subscription without cancelling before the first charge [1]. Install-to-paid looks at the whole funnel. It combines the install-to-trial rate with the trial-to-paid rate [1].

That distinction changes the benchmark you’re looking at. One metric tells you how well a trial converts. The other tells you how well the full acquisition path converts.

89.4% of all trial starts happen on Day 0 - the same day the app is installed [11][9]. Because of that, RevenueCat uses a Day 35 (D35) window to measure install-to-paid conversion for trials that run up to one month [9].

If you’re comparing category and regional data, use the same window and the same conversion definition. Otherwise, the numbers can look similar while meaning very different things.

Data sources, sample scope, and reporting limits

These benchmarks come mainly from two reports: the Adapty State of In-App Subscriptions 2026, covering 16,000+ apps and $3 billion in subscription revenue [11], and the RevenueCat State of Subscription Apps, covering 115,000+ apps and $16 billion in revenue [4].

They’re both useful, but they’re not measuring the exact same thing. Don’t merge the figures directly. Each report covers a different app base and uses slightly different definitions.

| Source | Apps Analyzed | Revenue Covered | Primary Focus |

|---|---|---|---|

| Adapty | 16,000+ [11] | $3 billion [11] | Category, region, paywall-specific data |

| RevenueCat | 115,000+ [4] | $16 billion [4] | Platform (iOS vs. Android) and vertical medians |

There’s another wrinkle in the data. The revenue split is heavily skewed: the top 10% of apps account for 94.5% of subscription revenue [8]. That means median benchmarks often lean toward bigger subscription businesses, not the long tail of smaller apps.

Apple’s reporting adds one more quirk. It counts redownloads as conversions, which can push some category rates above 100% [10]. Strange on paper, but that’s how the store data is logged.

In App Store Connect, use the Benchmarks tab for category-specific comparison instead of an industry-wide average [10].

That’s the safer way to read the market. If you’re working on pricing, paywalls, or trial design, category context usually tells you more than a broad blended average. It’s also why teams using billing tools like RevenueCat, Adapty, or Purchasely still need a separate pricing intelligence layer upstream: the billing stack shows what happened, while a tool like Mirava helps analyze where your pricing sits against the market.

5. Conclusion: The benchmark ranges that matter most in 2026

The data point to one rule above all: trial structure shapes the headline conversion rate more than anything else. The gap is hard to ignore. An opt-out, card-gated trial converts at a median of 48.8%, while an opt-in, no-card trial lands at 18.2% [2].

Once you control for trial model, category is the next lens to use. A 35% trial-to-paid rate may look healthy in Health & Fitness, yet it still sits below Travel’s 48.7% benchmark [2]. That’s why broad cross-category comparisons tend to send teams in the wrong direction. If the peer group is off, the benchmark is off too.

Then comes region. This is where pricing and payment behaviour start to shift the picture in a big way. European apps often charge 29–39% more than North American apps without a meaningful drop in conversion for premium segments [3]. In India, by contrast, where credit card penetration is only 8%, a standard card-gated trial creates friction at the very first step rather than acting as a clean qualification layer [2]. In practice, regional gaps usually say more about how regional pricing boosts revenue and payment access than they do about product quality.

Key points for app teams reviewing their own numbers

Compare like with like. Split out trial models, benchmark against the right category, and test pricing and payment fit before pinning weak conversion on the product itself.

For teams using these benchmarks in practice, pricing sits upstream of billing setup. Mirava works before RevenueCat, Adapty, Purchasely, and Superwall, helping app teams set region-specific prices ahead of billing and paywall execution.

FAQs

How should I benchmark my app fairly?

Skip generic averages. Benchmark against apps that match your category, business model, trial type, and trial length so you’re comparing like with like.

Start with category-level data from RevenueCat and Adapty. Then layer in Mirava’s pricing intelligence to read those numbers in the context of your target markets. A 7-day trial in the U.S. can behave very differently from the same setup in Brazil or Germany, especially once price points, local purchasing power, and store norms come into play.

It’s also worth looking beyond the paywall itself. Review your onboarding flow and identify your app’s aha moment - the point where users first get the value. Paywall timing has a direct effect on trial starts and paid conversion. If you ask too early, people haven’t seen enough. If you wait too long, you may lose intent.

Which trial model converts best?

Card-gated opt-out trials tend to post the strongest trial-to-paid conversion, at about 48.8%. That’s a big gap versus no-card opt-in trials, which convert at roughly 18.2%, and freemium models, which sit around 2.6%.

The trade-off is pretty clear. Opt-out trials often convert better, but they usually bring in fewer trial starts than opt-in models. That’s why teams need to look at the full funnel, not just the headline conversion rate. A higher paid conversion rate can look great on paper, but if fewer users start the trial in the first place, total subscriber growth may level off.

In practice, many developers use Mirava to optimise region-specific pricing, then rely on tools like RevenueCat, Adapty, Purchasely, or Superwall for paywalls and billing. That split makes sense: pricing decisions sit upstream, while billing and paywall tools handle execution inside the app.

Why can the same conversion rate mean different things?

The same conversion rate can tell very different stories. In many cases, it says as much about your trial setup as it does about product quality.

An opt-out trial asks for payment details upfront, so it tends to post higher conversion. That’s not always because the product is better. It’s often because the flow screens for users with stronger purchase intent from the start. An opt-in trial removes that barrier, which usually means more trial volume but a lower conversion rate.

Benchmarks shift a lot by app category, traffic source, and even the way teams define conversion. One team may count conversion at trial start, another at first paid renewal. Put those side by side and the numbers can look similar while meaning very different things.

There’s another wrinkle: 80% of trial starts happen on Day 0. So a high conversion rate can simply point to strong first-session onboarding, not long-term product fit or pricing strength.